The merger of companies into a group or business units with different service ranges under one organizational roof can have a wide variety of reasons.

Management and various services are often centralized. Sharing systems and personnel should lead to greater efficiency and better utilization than if each company, operation or business unit does everything itself and staffs each function independently. These synergies reduce operational management costs. This is offset by the complexity costs of organizing and managing headquarters.

When buying and selling companies, it is important to compare the savings from synergy effects with the complexity costs in order to make an economically sound decision.

In the case reported here, our customer was active in two business areas of the real estate industry:

- In the property development sector, he wrote strongly fluctuating results typical for the industry.

- In his service line (property management, brokers, janitor services), he had a constant profit situation with significantly lower sales/services.

Accounting, controlling, personnel services and IT were centralized in the holding company.

For strategic reasons, the group of institutional shareholders sought to sell the company as a whole. However, the current unsatisfactory earnings situation of the property development business made a short-term sale seem unattractive. The question therefore arose of initially selling only the service business. However, the Chief Executive Officer with overall responsibility for the company was opposed to this proposal. He justified this with the loss of synergy effects in administration. No quantitative analysis of this was available.

The advisory board of the shareholders then commissioned us to analyze and evaluate synergy effects and complexity costs. For this purpose, HC first analyzed the actual cost structures of the Group. The two operating divisions were largely separate. Relevant overlaps existed in the areas of management, accounting, controlling, EDP, financing as well as in the real estate used jointly for administrative activities.

The following exemplary findings emerged from the analysis based on interviews, hourly records and accounting vouchers:

- The chairman of the management board was appointed in all three companies. One person was additionally appointed as managing director in each division and in the holding company.

- The accounting department essentially worked separately for the individual business units under a common head – whose function thus meant certain synergy effects. Costs of complexity resulted in the holding company from the accounting material for service allocations to only a limited extent. Increased external costs resulted from the preparation of the annual financial statements of the holding company and, in particular, consolidated financial statements.

- In IT, the operating software products used in the business areas differed considerably and were clearly allocable. Synergy effects arose in user support for hardware and operating systems. Complexity costs resulted from proprietary consolidation software.

- The real estate was used by all three divisions.

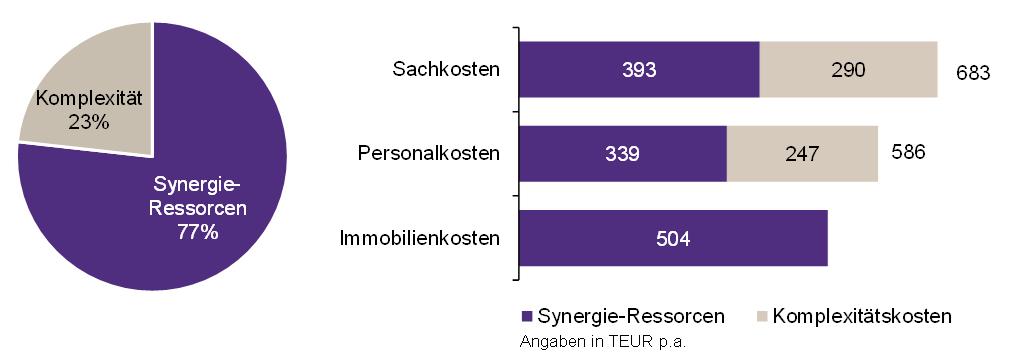

In a first step, the administrative costs were divided into clearly allocable and not clearly allocable costs. In the context of divisional contribution margin accounting, these are divisional direct costs and Group overheads. This first step resulted in the following breakdown:

Kostenstruktur der Verwaltungskosten

In order to be able to determine the synergy effects and complexity costs further on, the next step was to break down the costs for shared resources that could not be clearly allocated and those that resulted solely from the complexity of the group structure:

Nicht eindeutig aufteilbaren Verwaltungskosten:

Komplexitätskosten und produktiv für die Sparten genutzte Synergie-Ressourcen

The splitting of the two areas and establishment of a central administration resulted not only in synergy effects, but also in complexity costs of EUR 537 thousand for the central administration.

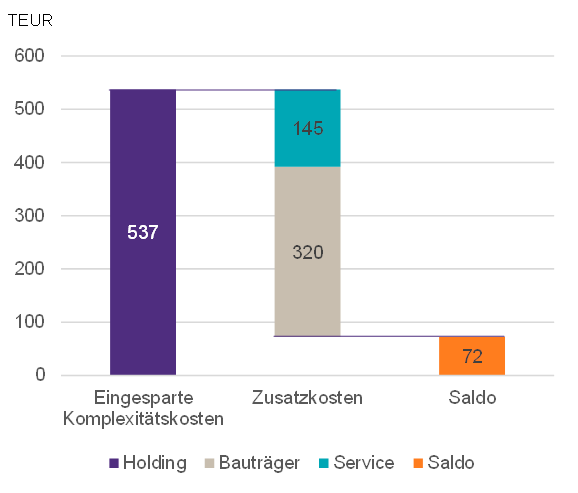

In the next step, the synergy effects from the joint use of resources with the complexity costs were analyzed further. To this end, the processes and quantity structures of the administrative activities were first determined if the administrative services were provided independently by the business units. This revealed additional requirements with corresponding additional costs:

- All parties involved wanted to see the respective management teams staffed with two people each.

- In the IT area, the separation of administration required additional manpower.

- The real estate was usable for both areas, but in the event of a separation, this would require construction measures that were quantified at a one-time cost of EUR 50 thousand.

This resulted in additional costs of EUR 465 thousand per year:

Gegenüberstellung von eingesparten Komplexitätskosten und

Zusatzkosten im Fall des Asset-Deals

If the administrative services were provided independently, this would result in additional costs of EUR 465 thousand from the elimination of synergies, but these would be offset by savings of EUR 537 thousand from the elimination of complexity costs. The one-off costs of the separation could already be covered from the difference in the first year.

The result led to a clear decision in favor of the partial sale of the services business, in line with the strategy originally envisaged.

Thus, the detailed identification and consideration of complexity costs, had a significant impact on the strategic decision.

The case study shows a relatively small group of a holding company with two operating subsidiaries. Synergy effects increase with the number of companies in a group, but so do complexity costs.

Complexity costs or their underestimation can also play a significant role in the acquisition or merger of companies. For a variety of reasons, potential synergies are often viewed very optimistically and complexity costs are underestimated.

The neutral analysis and evaluation of synergies and complexity costs is therefore an important piece of information for economic decisions, both when buying within the framework of DD and when selling.

HANSE Consulting can support you in analyzing these important issues based on its experience and competencies in controlling and the analysis of corporate processes and structures.

Talk to us.

Feel free to contact us, we look forward to your inquiry! The experts at HANSE Consulting are there for you.